Statutory Residence

Flow Chart for Individuals, alive during the entire tax year

Some important definitions

Calculation of Days Spent in the UK

You are considered to have spent a day in the UK if you are here at the end of the day (midnight).

This is subject to:

1. The deeming rule which will count certain days even though you were not here at midnight

2. Transit days

3. Time spent in the UK due to exceptional circumstances — those days may not count towards the total day count for certain parts of the Statutory Resident Tests

Home in the UK

An individual will be regarded as resident under the 2nd automatic test if the individual has a home in the UK which is available for 91 consecutive days, 30 of those days fall in the tax yearand they are present in that home for at least 30days at any time that year. The individual should also either have no home overseas or if they do be present in it for less than 30 days in the tax year.

Working full time in the UK

Work more than 35 hours a week on average in the UK over a period of 365 days. During the 365 day period there are no significant breaks from work and more than 75% of the working days are carried on in the UK with a least one working day in the tax year. A working day is any day on which at least 3 hours work is performed.

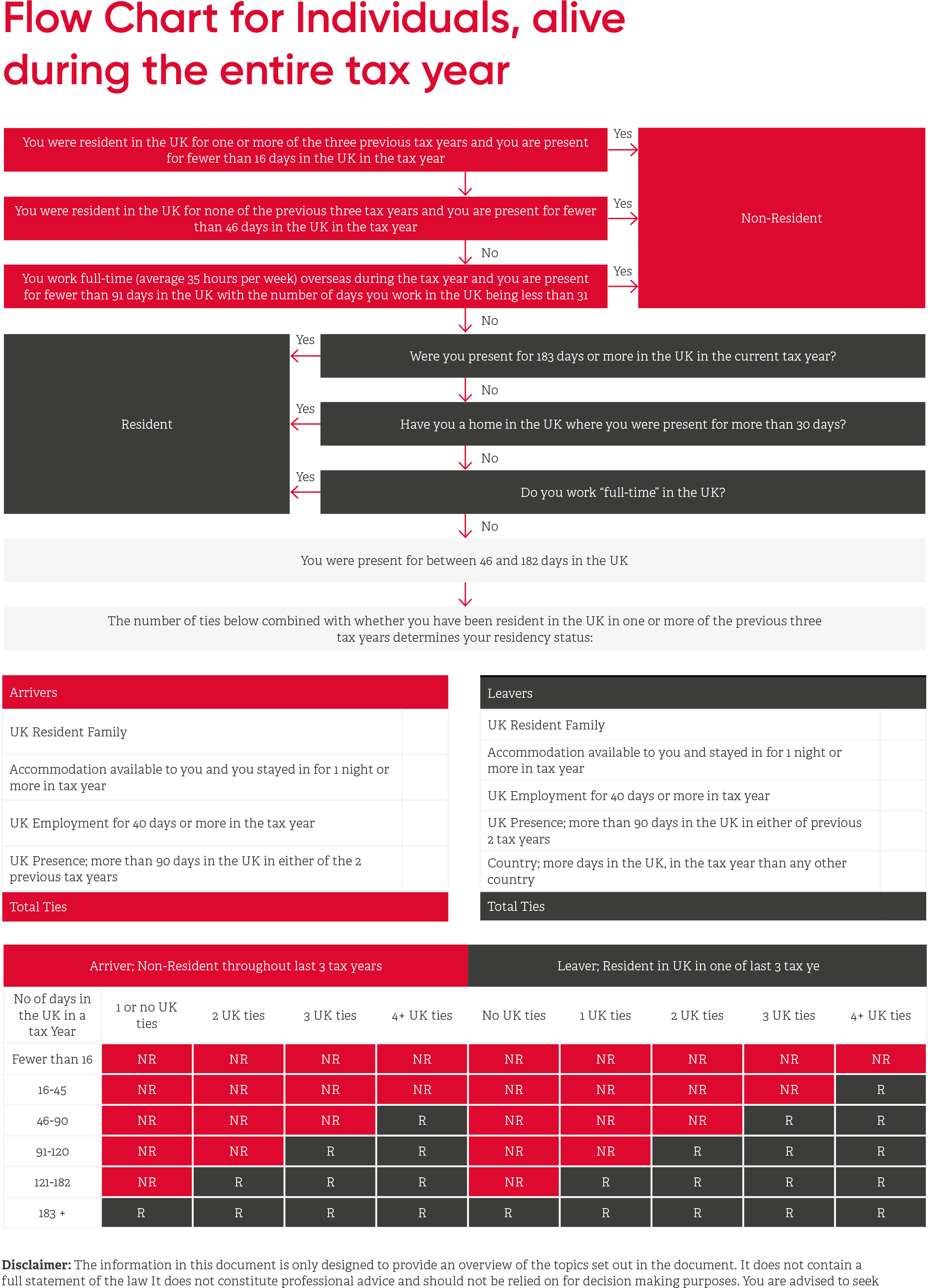

Sufficient Ties

The residence of individuals who do not fall within either the automatic overseas tests or the automatic UK residence tests, iis determined by the sufficient ties test. This test considers both the number of days spent in the UK and the number of the individual’ “ties” to the UK.

Generally, the fewer ties that you have, the longer you can spend in the UK without becoming UK resident. The ties to be considered include:

- a family tie

- an accommodation tie

- a work tie

- a 90 day tie

- a country tie )only for “leavers”

Ties are specifically defined. For example:

Accommodation Tie

It should be noted that an individual who has accommodation available to them for a continuous period of 91 days and spends at least one night at this accommodation, has created a tie. Should the accommodation be that of a close relative and 16 or more nights are spent, this also creates a tie.

Let us Introduce Ourselves

To find your nearest office or get in touch with one of our specialist advisors to see how we can help your business, please go to our contact page.